6 Ways How Surety Bonds are Insurance

6 Ways How Surety Bonds are Insurance

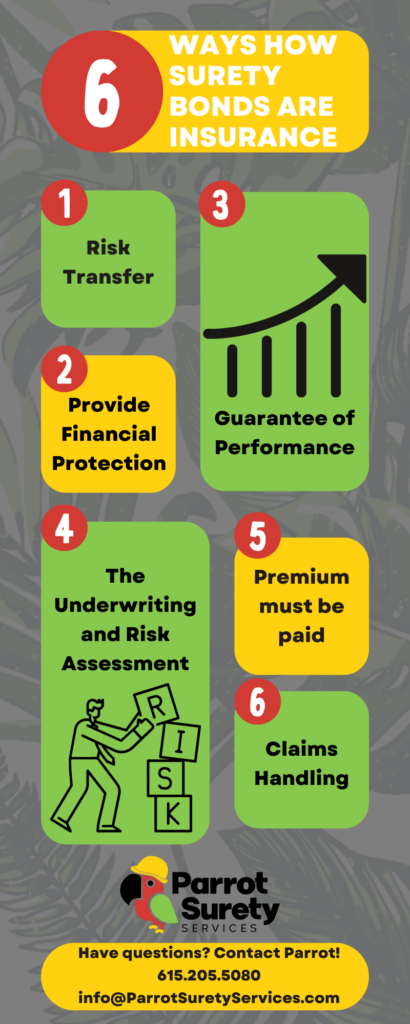

| Surety bonds are often considered a form of insurance because they involve a transfer of risk in which a surety company provides financial protection or guarantees the performance of certain obligations. Here are the key reasons why surety bonds are often classified as insurance: → Risk Transfer: Like traditional insurance, surety bonds involve the transfer of risk from one party to another. In the case of surety bonds, the risk is transferred from the obligee (the party requiring the bond) to the surety company. The surety company assumes the financial risk associated with the bonded party’s failure to fulfill their obligations. → Financial Protection: Surety bonds provide financial protection to the obligee in case the bonded party fails to meet their contractual or legal obligations. If a loss occurs due to the bonded party’s non-performance, the surety company compensates the obligee up to the bond amount, ensuring that the obligee does not suffer financial harm. → Guarantee of Performance: Surety bonds guarantee the performance of specific obligations or responsibilities. They assure the obligee that the bonded party will fulfill their contractual commitments, adhere to regulations, or meet legal requirements. If the bonded party fails to fulfill their obligations, the surety company may step in to remedy the situation or provide compensation to the obligee. → Underwriting and Risk Assessment: Surety companies assess the risk associated with providing the bond by evaluating the financial stability, creditworthiness, and qualifications of the bonded party. This underwriting process is similar to how insurance companies assess risks before issuing insurance policies. → Premium Payment: The principal (the party obtaining the bond) pays a premium to the surety company for issuing the bond. This premium serves as the consideration for assuming the risk and providing the financial guarantee. The premium amount is based on factors such as the bond type, bond amount, and the risk profile of the principal. → Claims Handling: If a claim arises due to the bonded party’s non-performance, the obligee can make a claim against the surety bond. The surety company will investigate the claim and, if valid, provide compensation to the obligee up to the bond amount. This claims handling process is similar to how insurance claims are handled. While surety bonds share certain similarities with traditional insurance, it’s important to note that there are also differences in how they operate, the parties involved, and the nature of the risks being covered. Most insurance agents are not experienced or familiar with surety. Our team at Parrot Surety Services is here for all of your surety bond needs and questions. Contact any member of our team for dedicated surety expertise and support! |

| Surety bonds are often considered a form of insurance because they involve a transfer of risk in which a surety company provides financial protection or guarantees the performance of certain obligations. Here are the key reasons why surety bonds are often classified as insurance: → Risk Transfer: Like traditional insurance, surety bonds involve the transfer of risk from one party to another. In the case of surety bonds, the risk is transferred from the obligee (the party requiring the bond) to the surety company. The surety company assumes the financial risk associated with the bonded party’s failure to fulfill their obligations. → Financial Protection: Surety bonds provide financial protection to the obligee in case the bonded party fails to meet their contractual or legal obligations. If a loss occurs due to the bonded party’s non-performance, the surety company compensates the obligee up to the bond amount, ensuring that the obligee does not suffer financial harm. → Guarantee of Performance: Surety bonds guarantee the performance of specific obligations or responsibilities. They assure the obligee that the bonded party will fulfill their contractual commitments, adhere to regulations, or meet legal requirements. If the bonded party fails to fulfill their obligations, the surety company may step in to remedy the situation or provide compensation to the obligee. → Underwriting and Risk Assessment: Surety companies assess the risk associated with providing the bond by evaluating the financial stability, creditworthiness, and qualifications of the bonded party. This underwriting process is similar to how insurance companies assess risks before issuing insurance policies. → Premium Payment: The principal (the party obtaining the bond) pays a premium to the surety company for issuing the bond. This premium serves as the consideration for assuming the risk and providing the financial guarantee. The premium amount is based on factors such as the bond type, bond amount, and the risk profile of the principal. → Claims Handling: If a claim arises due to the bonded party’s non-performance, the obligee can make a claim against the surety bond. The surety company will investigate the claim and, if valid, provide compensation to the obligee up to the bond amount. This claims handling process is similar to how insurance claims are handled. While surety bonds share certain similarities with traditional insurance, it’s important to note that there are also differences in how they operate, the parties involved, and the nature of the risks being covered. Most insurance agents are not experienced or familiar with surety. Our team at Parrot Surety Services is here for all of your surety bond needs and questions. Contact any member of our team for dedicated surety expertise and support! |